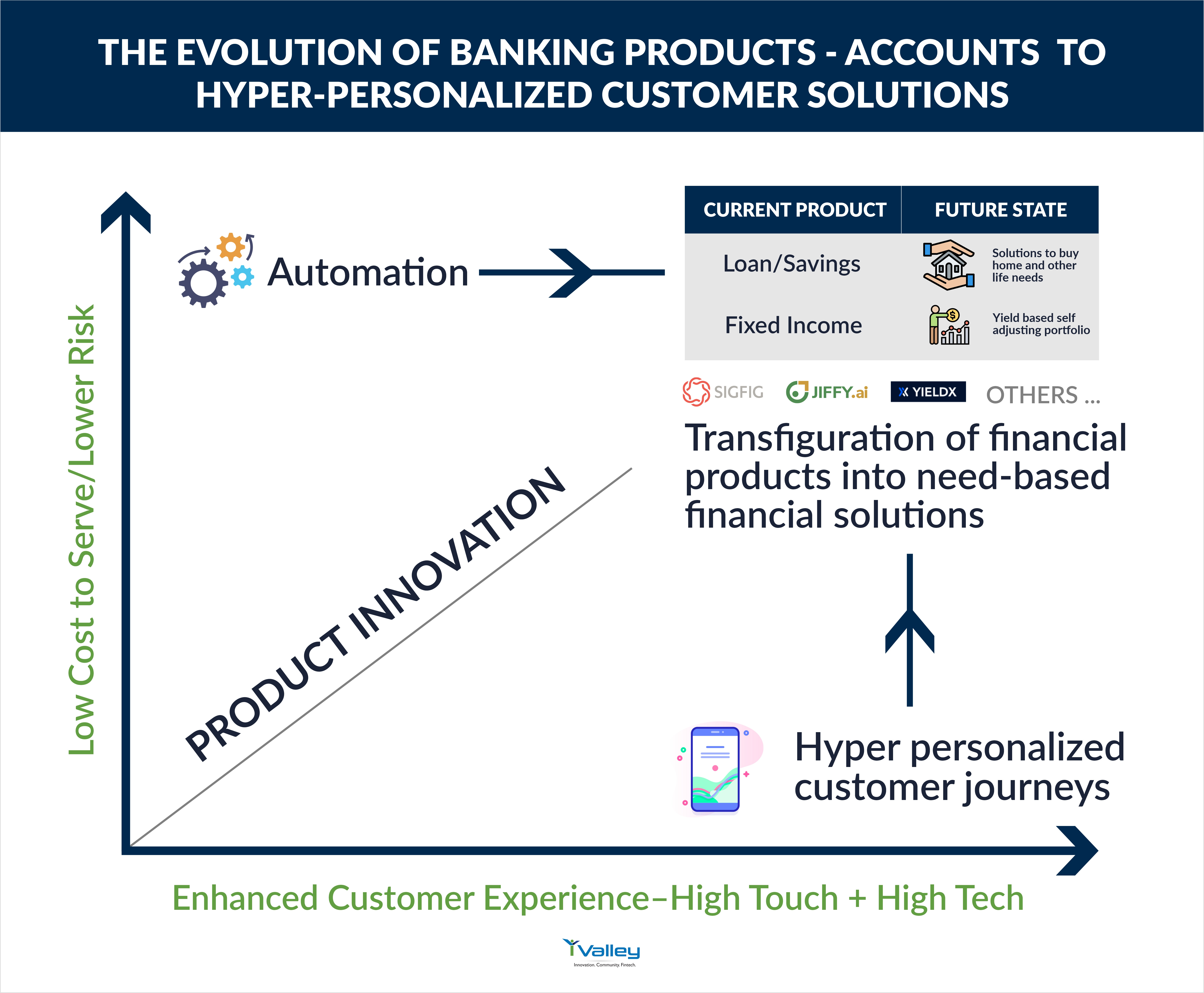

Fintechs Transfiguring Financial Products to Goal-Based Financial Solutions

Preview of the next generation of neoFin platforms and hyper-personalized apps

HI FINTECHTALKERS,

I sat down with Mike Sha (CEO of SigFig), Michael Partnow (Head of Wealth at Jiffy.AI) and, Adam Green (CEO of YieldX), last week on the FINTECHTALK Show (http://www.fintechtalk.co) to talk about the next generation of platforms and hyper-personalized apps in financial services. A succinct summary of the conversation by the Fintech Elder and our editorial epilogue in this edition of eFINTECHTALK.

The next generation of fintechs are transforming the industry by not only digitizing the customer journey but transfiguring the financial products to goal-based solutions for consumers and institutions. It’s a perfect storm of enhanced customer experience, reduced cost to serve, and product innovation.

Join me for our show next week where we feature Crypto startups from around the world and how they are disrupting the internet and finance: Centrifuge, Rsk, Acala, Unizen, Concordium, and more. Wed July 14th at 12 pm Pacific

Join me live at https://www.clubhouse.com/event/xoNrOEyl ((use link to save to your calendar)

iValley is a 3rd generation startup factory, sculpting the future of fintech and crypto-economy. To join iValley click here

Enjoy and always Be in the Know,

Paddy Ramanathan

Founder of iValley (www.ivalley.co) and

Host of the FINTECHTALK™ Show (http://www.fintechtalk.co)

Crypto Economy Startups from Around the World

July 14, Wednesday | 12: 00 PM PDT (use link below to save to your calendar)

How Small Business Focused Fintechs are Changing the Game?

July 28, Wednesday | 12: 00 PM PDT (use link below to save to your calendar)

NeoFin Platforms and Hyper-apps: Hyper About Customers and Fixed Income

Recap of the FINTECHTALK Show of June 30th by the Fintech Elder

Reams of Management thought have gone into developing persuasive cases for why we ought to focus on customers.

It sounds politically correct. It sounds inspiring. It sounds wonderful.

But again and again, we don’t actually get it.

Our organizations are structured around products and services. We find clever ways to persuade customers to spend money on what we think is right for them.

And in that, is our failure.

We never ask what the customer really wants. Is the product or service simply a means to get somewhere else, just beyond the horizon?

With such deep thoughts, I sat down at a quiet place in the digital shadows, nursing a coffee, to hear the views of some pretty cool guys at the FINTECHTALK Show on Neofin Platforms and Hyperapps on Clubhouse on June 30th.

Sounds Greek, did you say? You couldn’t be more wrong. Read on.

Let’s start by recalling that Fintech cleaned up existing customer journeys in Phase 1 - made it easier to pay, get a loan, and providing Robo-advising. The next generation of products would take it to the next level by eliminating the traditional banking metaphor of accounts, loans, etc to needs and goals of people and businesses and institutions like I need to get home, I need to get a yield on my investments to get to college and so on.

As usual, the ebullient Paddy Ramanathan, CEO of iValley, a 3rd generation Fintech incubator, moderated the session with elan. Sharing the stage were

Mike Sha, CEO, and Co-founder at SigFig, which touts itself as Build an intelligent, tax-efficient, diversified portfolio for a fraction of the cost of traditional advisors.

Michael Partnow, Head of Wealth Management at JIFFY.ai. They work on Intelligent Automation for Business Transformation

Adam Green, Co-Founder and Chief Executive Officer at YieldX, whose banner proclaims that they revolutionize fixed income investing with an end-to-end digital platform that powers personalization at scale.

With very impressive – and diverse - achievements behind them, these gentlemen clearly had some serious credibility. But what seemed a great common ground was that was genuine customer obsession, both individuals and institutions.

Mike observed his stint at Amazon gave him a perspective about how technology could take customer obsession to a different level. His firm now works with firms that want a better customer-centric investment product.

Michael’s perspective was a little different: his company wants to radically automate processes and place them in the hands of users. Throwing disruptive technology at a problem won’t solve it, as certain processes can’t be changed easily. That’s a big deal, which I will refer to again a bit later.

Adam’s orientation was about applying process automation to Fintech dealing with Fixed Income issues. Adam spent time at Bank of New York and Citadel and knows a thing or two about Fixed Income*.

(*Fixed income is an investment approach focused on the preservation of capital and income. It typically includes investments like government and corporate bonds, CDs, and money market funds. Fixed income can offer a steady stream of income with less risk than stocks.)

Distilled Fact: no one really gets excited about Financial Products. They see them as a means to get to specific ends. And so, while this by itself sounds obvious, the industry hasn’t really calibrated itself accordingly and build products that help users understand how to get to where they want to go. The legacy model of engagement involved meeting managers at branches, which has immense value. Has the pandemic era induced a consultative approach, giving rise to hyper-personalized products?

What did President Reagan say? “Mr. Gorbachev, tear down the wall!”

Customers don’t really silo their money (great point!), but banks segregate their products based on how they are internally organized, which is quite a pity. Customers need to be treated as one entity instead of four, depending on banking products, and regulatory and compliance complexities need to be embedded. This high-touch approach is important in critical life event financial decision making.

That’s profound!

Adam’s efforts involve doing that on the institutional side. Financial Product owners are seeking answers across the value chain, by democratizing legacy products and delivering them.

The whole value chain is very complex, and automating would be a big deal. As Michael put it, the Fixed income world - touching 200 trillion dollars in movement - is quite opaque and each component has its own set of layers and regulations.

YieldX is pushing integrated banking, emphasizing personalized, engaging experiences. Can all asset classes and segments be made available on one screen, irrespective of back-end processes, regulations, and compliance realities?

And that’s not easy, as Mike reminded us. Many of the tools were built for a different time when they were just interfaces to a mainframe. And so, products have sat around for decades, disregarding simplicity and usability. It’s not that easy to simply pull away from legacy technology that has factored in regulations and compliance processes.

A profound thought: good design ought to mean it’s easy to learn and less about technology and more about getting basics right. Yes!

Michael reminded us that no one wants to automate a broken process. Because: what’s the point? He alluded to what Jim Henson said prophetically in the 70s. Machines should work, people should think. Those words ring true even today.

This is why it is so important to partner with the CIO, CTO, and the user, and truly understand what is firmly here now is that business drives technology.

And co-create.

I liked Adam’s bold statement that he insists UI guys ought not to come from a financial background. It showed a lot of sensitivity.

Paddy’s query about what innovation in the capital market is being seen today got a thoughtful response. Michael felt the real focus of innovation and automation in on the front and middle office, where, for instance, trade order processing is still manual and high risk.

Fixed Income margins are not easily understood, observed Adam. The API approach enables the development of a better risk profile in an automated way, especially when you need to get the regulatory model right. Defi will go on the mainframe, utilizing the blockchain to deliver products. That’s pretty visionary if you think about it!

And who do you sell to at Financial Institutions? Here too, these exemplar companies believe a consultative approach is an idea, emphasizing listening. And as Michael said, the economic buyer today is a combination of technology and business savvy, who does get that automation of processes is the best way to truly “get” the Fixed Income customer.

The pandemic has really had an impact on the way people think of the customer. Many changes will be permanent. Automation has become an obvious necessity. That’s perhaps a blessing in disguise!

“The customer is King”. Yes, it’s a revolution for the Fixed Income world. All hail Neofins and Hyperapps for making it happen!

The Fintech Elder is the ultimate Fixed Income customer. No one knows who he is.

EPILOGUE

To join iValley as it sculpts (build, write, and talk) the future of fintech and future economy - click here.

Connect with us!

iValley Innovation Center

11040 Bollinger Canyon Rd, E-909

San Ramon, CA 94582,

The United States.

Phone: +1 925-575-7832