The AI Execution Economy

How AI Is Moving from Productivity Tools to Enterprise Operating Leverage - from software workflows to the agent-orchestrated enterprises

Table of Contents

I. What’s Actually Breaking

II. AI Is Becoming the Enterprise Execution Layer

III. From Model Wars to Margin Wars

IV. The Enterprise AI Transformation Framework

V. The Rise of AI-Native Companies

VI. How iValley Helps Enterprises Navigate AI

In the first part of this series, we argued that crypto and SaaS are not merely correcting. They are being repriced inside a broader macro and structural reset.

Capital is rotating away from growth-at-any-cost models and toward businesses where AI can create measurable operating leverage.

In this second part, we look at the other side of that rotation:

AI is moving enterprises beyond the cloud-era playbook — from software-centric operations to agent-orchestrated execution, and from rented applications toward owned intelligence, workflow automation, and AI-native operating models.

The core thesis is simple:

The cloud era digitized workflows.

The AI era executes them.

Read Part 1 of this series here →

Why Crypto and SaaS are Drowning in the 2026 Reset - Part 1

The Shadow Swap Line: Why Bitcoin may have been the Central Bank’s Ultimate Insurance Policy

I. What’s Actually Breaking

The previous cycle was built on three assumptions:

Liquidity would remain abundant

Opex-heavy models would be rewarded

Software would be the dominant abstraction layer

All three are now under pressure.

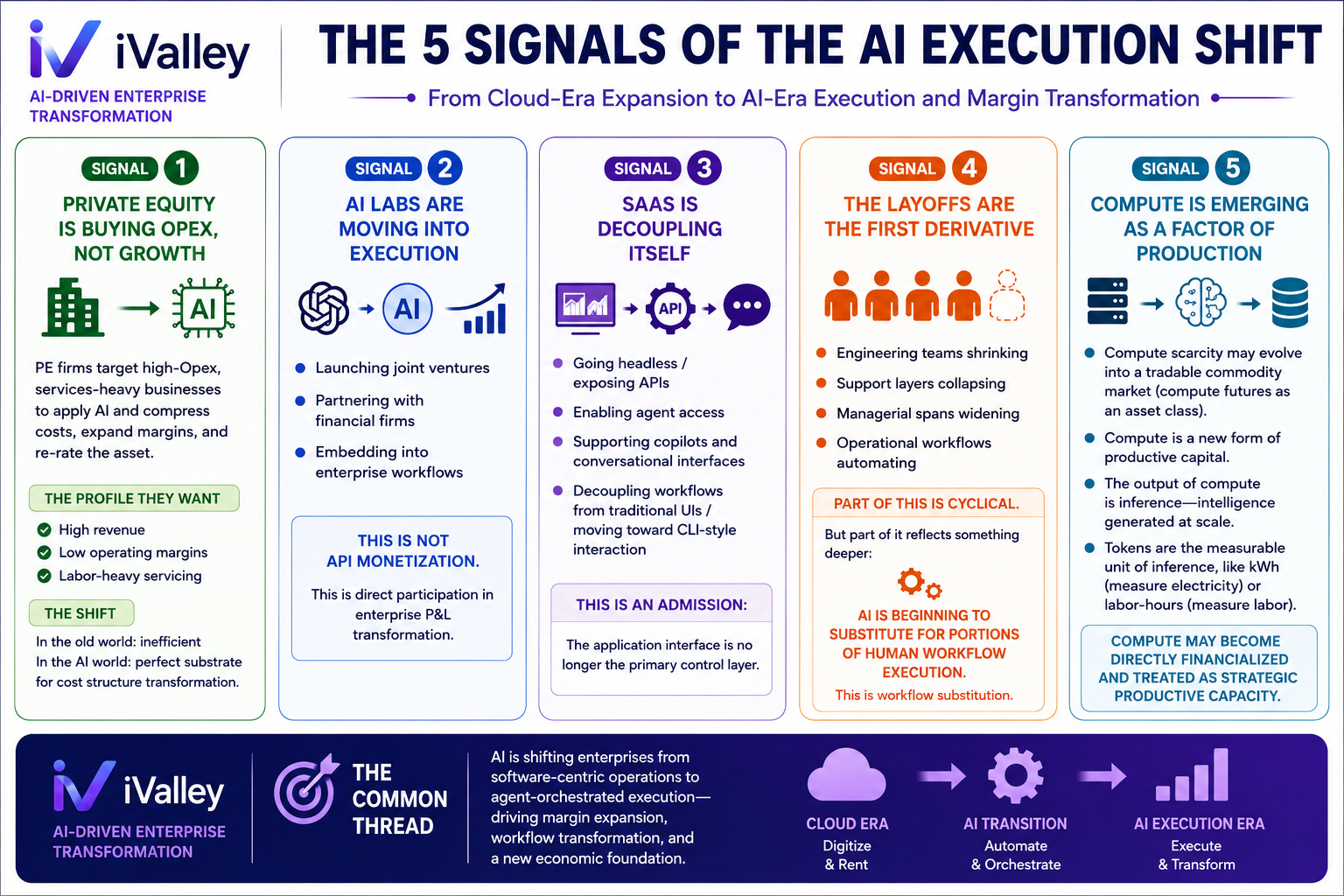

Signal 1: Private Equity Is Buying Opex, Not Growth

The acquisition of Global Business Travel Group (GBTG) by Long Lake Management is not a travel bet. Long Lake backed by General Catalyst and Alpha Wave, charter is to apply frontier AI to services-heavy industries, In plain terms: buy high-Opex businesses, use AI to compress operating costs, expand margins, and re-rate the asset

It is a cost structure transformation bet.

High revenue

Low operating margins

Labor-heavy servicing

In the old world, this profile was inefficient.

In the AI world:

It is the perfect substrate.

Signal 2: AI Labs Are Moving Into Execution

OpenAI and Anthropic are not behaving like infrastructure companies anymore.

They are:

Launching joint ventures

Partnering with financial firms

Embedding into enterprise workflows

This is not API monetization.

This is:

Direct participation in enterprise P&L transformation.

Signal 3: SaaS Is Decoupling Itself

Salesforce and others are:

Going headless/exposing APIs

enabling agent access

supporting copilots and conversational interfaces

decoupling workflows from traditional UIs/moving toward CLI-style interaction

This is adaptation.

But it is also an admission:

The application interface is no longer the primary control layer.

Signal 4: The Layoffs Are the First Derivative

Across tech:

engineering teams shrinking

support layers collapsing

managerial spans widening

operational workflows automating

Part of this is cyclical.

But part of it reflects something deeper:

AI is beginning to substitute for portions of human workflow execution.

This is:

Workflow substitution

Emerging Macro Thesis - Early Signal 5: Compute Is Emerging as a Factor of Production and Inference is the productive output

Larry Fink recently suggested that compute scarcity could evolve into a tradable commodity market — with compute futures potentially becoming an asset class.

That signal matters because AI is changing what constitutes productive capacity in the economy.

Compute is emerging as a new form of productive capital.

The output of that capital is inference — intelligence generated at scale.

Tokens become the measurable unit of that inference, similar to how kilowatt-hours measure electricity or labor-hours measure human work.

Compute may become directly financialized and treated as strategic productive capacity.

II. Connecting the Dots: AI Is Becoming the Enterprise Execution Layer

Individually, the five signals look disconnected:

PE firms buying services-heavy businesses

AI labs embedding into enterprise workflows

SaaS platforms exposing APIs and going headless

labor structures compressing

compute becoming strategic productive capacity

Together, they point to the same conclusion:

AI is moving from productivity tool to enterprise execution layer.

The cloud era digitized workflows.

The AI era orchestrates and executes them.

That is the structural shift.

In the SaaS era:

humans operated software.

In the AI era:

agents increasingly operate systems on behalf of humans.

This changes where enterprise value lives.

Why Programming Came First

AI did not begin with enterprises.

It began with code.

Because code is:

structured

deterministic

testable

verifiable

Agents could:

generate

validate

deploy

iterate

Vibe coding was not the destination.

It was proof that workflows themselves can become agent-executable.

That transition is now spreading into enterprises.

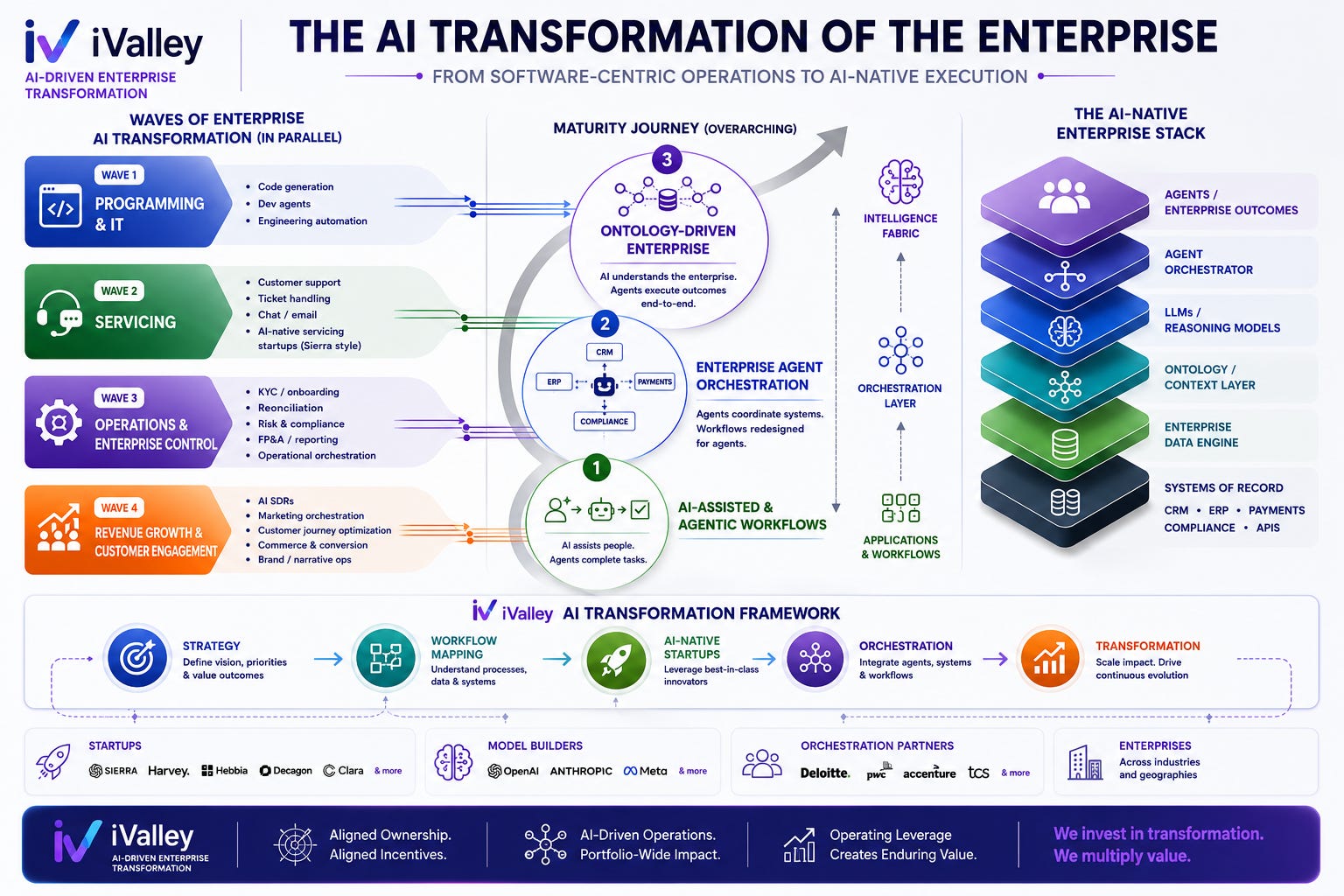

The Transformation Progresses in Waves

Wave 1 — Programming & IT

code generation

dev agents

IT automation

Wave 2 — Servicing

customer support

ticket handling

conversational workflows

This is already happening.

Sierra’s rise is an early signal that AI-native servicing layers may challenge legacy SaaS incumbents.

Wave 3 — Enterprise Operations & Control

AI moves into:

onboarding

compliance

reconciliation

FP&A

reporting

operational coordination

This is where enterprise operating leverage begins to materially change.

Wave 4 — Revenue & Customer Orchestration

AI expands into:

sales

marketing

personalization

commerce

customer engagement

narrative generation

The progression matters because enterprise AI adoption moves from:

deterministic workflows

toward:unstructured human coordination and reasoning.

That is the path from copilots to AI-native enterprises.

The current market is mostly pricing productivity gains.

But the real enterprise re-rating may happen when:

workflows become agent-native,

orchestration replaces interfaces,

and enterprises evolve from software-centric organizations to AI-native operating systems.

That is the transition explored in the rest of this piece.

From AI Experimentation to AI-Native Operating Leverage

The first phase of AI was about models.

The next phase is about workflow orchestration.

Enterprise leaders are moving past the question of whether to “use AI.” The real question is which workflows to transform first — and what architecture can move the organization from AI assistance to AI-native execution.

That is where iValley is focused.

We help enterprises identify high-friction, high-Opex workflows, evaluate AI-native partners, and move from pilots to measurable operating leverage.

The cloud era digitized workflows.

The AI era executes them.

As enterprises move from copilots to AI-native execution, the challenge is no longer whether to adopt AI — but where to transform first and how to orchestrate that transition. If you are navigating that journey, reach out to us at info@ivalley.co or schedule an exploratory conversation here.

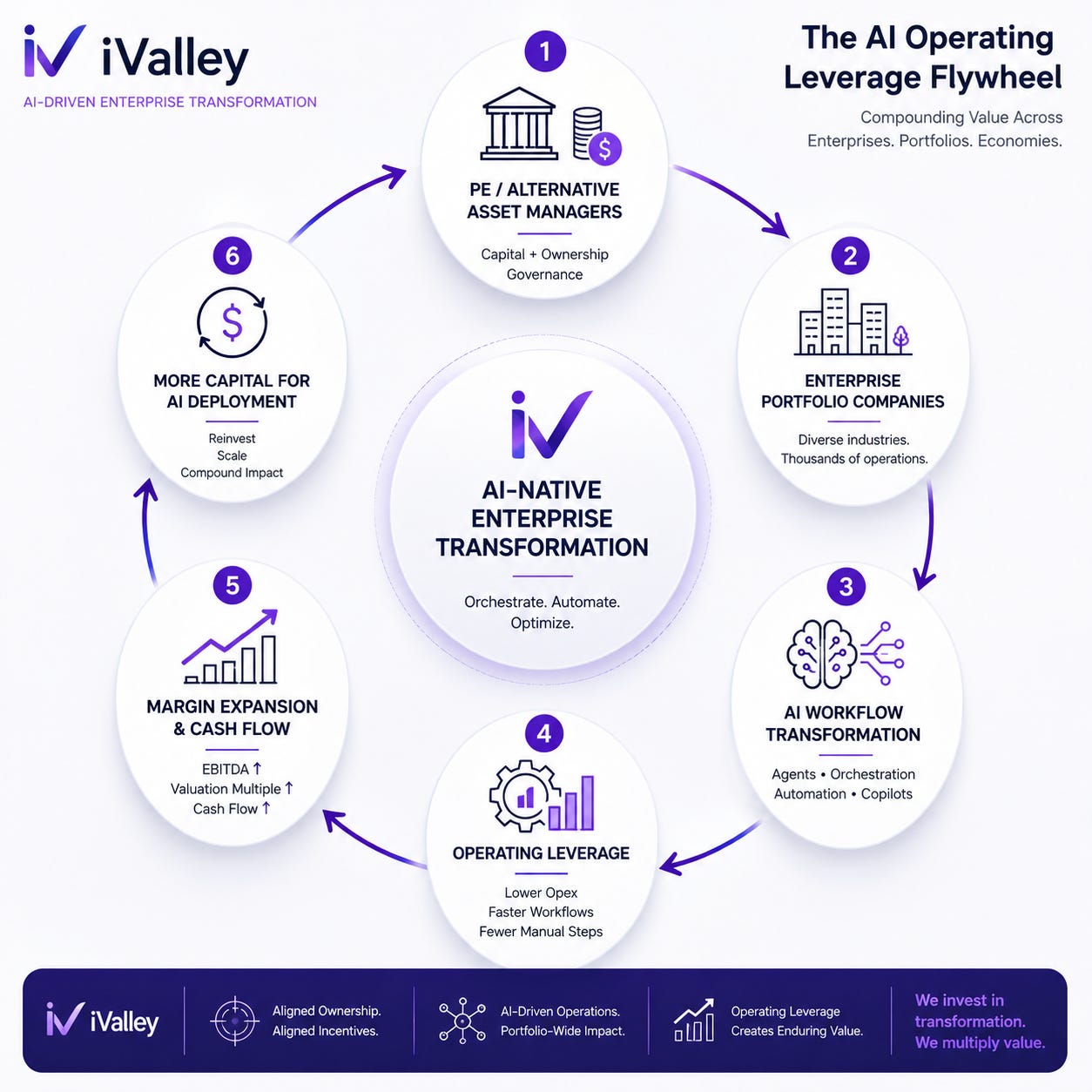

III. From Model Wars to Margin Wars

The Enterprise AI Flywheel

The recent partnerships between OpenAI, Anthropic, private equity firms, and alternative asset managers are not merely consulting or distribution deals.

The frontier labs are aligning with alternative asset managers because those firms control the largest concentration of transformable enterprise cash flows in the world.

They represent a structural alignment between frontier AI labs and the owners of enterprise operating economics.

Frontier AI labs and alternative asset managers are building a new enterprise flywheel where AI transformation compounds across portfolios, workflows, and operating margins.

The challenge is no longer whether enterprises should adopt AI.

The challenge is identifying which workflows should be transformed first, which operating models need to evolve, and how to move from experimentation to measurable operating leverage.

AI as a P&L Transformation Story

That is the transformation journey iValley is helping enterprises navigate.

Firms like:

Blackstone

Apollo Global Management

Brookfield Asset Management

Bain Capital

TPG

Hellman & Friedman

collectively own, finance, or influence thousands of enterprises globally.

Their returns depend on:

operating margins

labor efficiency

cash flow generation

EBITDA expansion

enterprise re-rating

That makes them natural partners for AI-native workflow transformation.

The first phase of the AI cycle rewarded:

chips

infrastructure

models

applications

The dominant metric was:

revenue growth.

But the next phase is different.

The focus is shifting toward:

workflow automation

operating leverage

labor substitution

enterprise orchestration

margin expansion

The dominant metric increasingly becomes:

EBITDA uplift per deployed AI dollar.

This is the transition from:

AI as a growth story

to:AI as a P&L transformation story.

Why PE and Alternative Asset Managers Matter

Private equity and alternative asset managers already influence boards, operating priorities, and transformation budgets across their portfolios.

That creates a powerful closed-loop deployment system:

AI models

enterprise distribution

workflow transformation

financing

operational enforcement

all aligned under the same economic incentives.

This is why OpenAI and Anthropic are moving beyond APIs and copilots into:

AI-native services firms

workflow transformation organizations

embedded deployment teams

The significance of these partnerships is not that AI companies are entering consulting.

It is that frontier AI labs are aligning themselves with the largest concentration of transformable enterprise cash flows in the world.

The AI stack is moving:

from software procurement

to:operating-model transformation.

And private equity firms may become one of the most important distribution channels for enterprise AI adoption globally.

IV. The Enterprise AI Transformation Framework

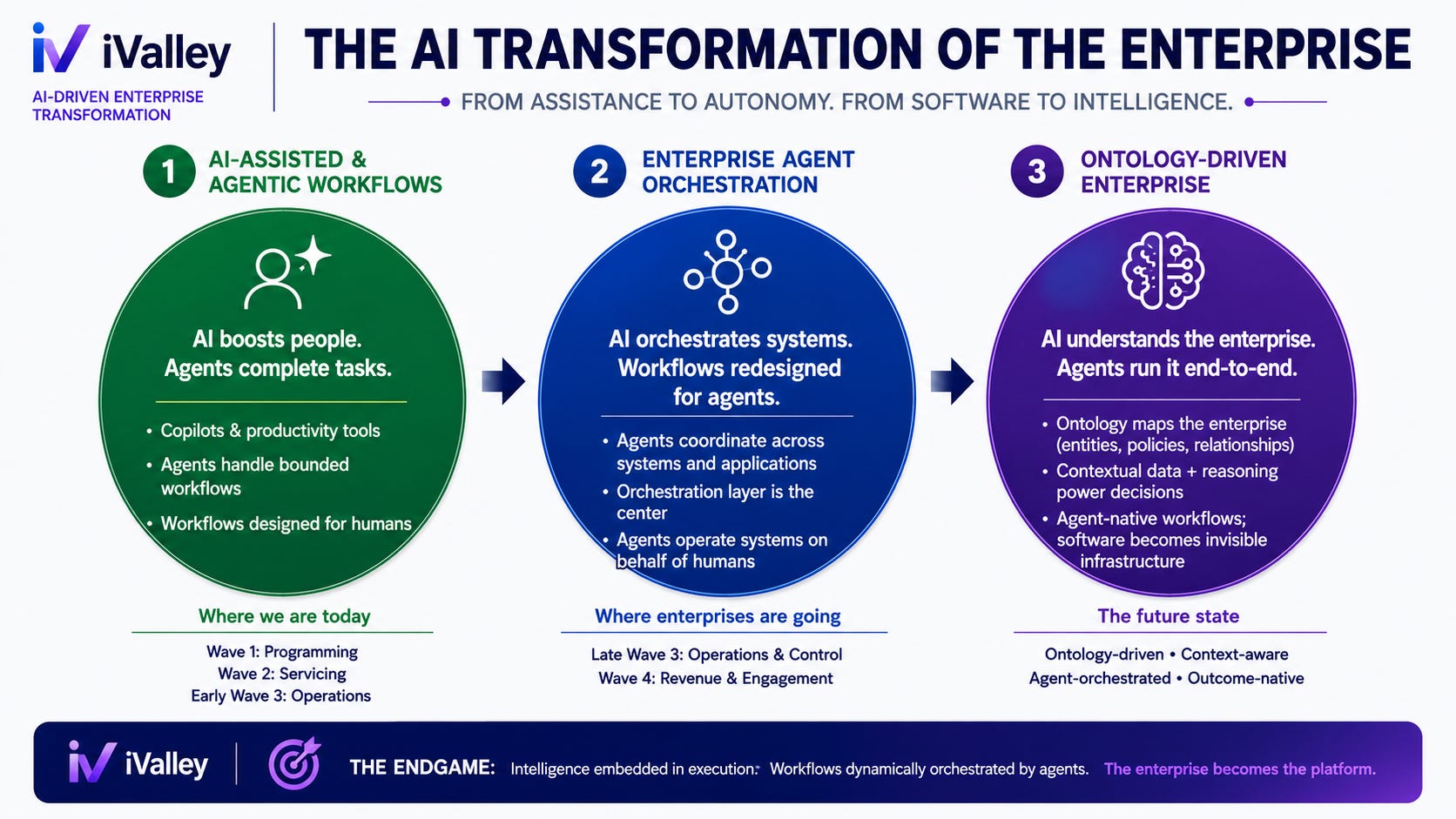

Enterprise AI transformation will not happen in one step. It will unfold in stages.

Stage 1: AI-Assisted and Agentic Workflows

This is where most enterprises are today.

AI starts by improving individual productivity through copilots, coding assistance, summarization, support augmentation, and content generation.

But the real shift begins when AI moves from assistance to execution.

Agents begin handling bounded workflows such as customer service, onboarding, reconciliation, compliance operations, reporting, and internal coordination.

This is where companies like Sierra operate today.

The key point is that these workflows are still largely designed for humans. Agents are being inserted into existing enterprise architectures rather than enterprises being redesigned around agents.

Stage 2: Enterprise Agent Orchestration

The next phase is enterprise orchestration.

Instead of adding copilots to existing workflows, companies begin redesigning workflows for agents themselves.

Agents coordinate across CRM, ERP, payments, compliance, ticketing, reporting, and operational databases. The workflow is no longer tied to a single application. It becomes an execution layer across systems.

This marks the shift from:

humans operating software

to agents operating enterprise systems on behalf of humans.

The winners in this phase will not simply have the best applications. They will orchestrate the best enterprise outcomes.

This is also why OpenAI, Anthropic, consulting firms, and AI-native integrators are moving deeper into services-heavy enterprise transformation. Strategically, they are trying to become part of the enterprise orchestration layer.

Stage 3: The Ontology-Driven Enterprise

The final stage is more architectural.

Today, software is still mostly built for humans: dashboards, forms, workflows, menus, and reports.

APIs, MCPs, and agent protocols give AI systems access to tools. But access is not the same as understanding.

Agents also need to understand what entities mean, how workflows relate, what policies govern decisions, which actions are allowed, and how the business actually operates.

That is where the ontology layer emerges.

The ontology becomes a machine-readable map of the enterprise — understood by both humans and agents.

In this model:

the ontology maps the enterprise

the data layer provides context

LLMs provide reasoning

agent orchestrators execute workflows across systems

This is the path toward context-aware, ontology-driven, agent-orchestrated enterprises.

The endgame is not chatbots.

It is enterprises where intelligence is embedded into execution, workflows are dynamically orchestrated by agents, and software increasingly recedes into invisible infrastructure behind business outcomes.

We will explore this ontology-driven enterprise architecture in a future FINTECHTALK paper.

V. The Rise of AI-Native Companies

The AI Native Landscape and characteristics

This is where disruption enters.

AI-native companies are not simply building better SaaS products.

They are attacking specific enterprise functions and rebuilding them around AI-native execution.

Sierra starts with customer service.

Others are emerging around software development, healthcare, legal workflows, financial operations, robotics, search, and enterprise automation. I recently had a X thread on how Sierra could become the AI Native company that disrupts current CRM.

These companies do not begin with:

a product,

a UI,

a module,

or a dashboard.

They begin with:

a workflow,

a business outcome,

a human task,

or an enterprise function that can be learned, reasoned through, and executed.

That gives enterprises a new build-versus-buy question.

Do they build their own agentic orchestration layer internally?

Or do they buy from AI-native companies that specialize in one function, such as servicing, compliance, sales, engineering, or healthcare operations?

The AI Native vs the AI Enabler

In the near term, many AI-native companies will look like enterprise vendors.

They will sell into existing corporations and sit across legacy systems: CRM, ticketing, policy documents, knowledge bases, payments, risk systems, and data warehouses.

But the longer-term opportunity is larger.

Some AI-native companies will not remain software or service providers to enterprises.

They will become new enterprises themselves.

That is what happened in the digital transformation era.

Uber was not just software for taxi companies.

Airbnb was not just software for hotels.

Amazon was not just software for retailers.

They used digital infrastructure to create new operating models.

AI-native companies may follow the same pattern.

A company that begins as an AI healthcare workflow platform could become an AI-native healthcare provider with a real-time patient twin.

A company that begins as an AI banking operations layer could become an AI-native challenger bank.

A company that begins by automating enterprise workflows could become an AI-native corporation — built from the ground up with agents, models, context, and orchestration instead of departments, applications, and manual coordination.

That is the real disruption.

SaaS digitized enterprise workflows.

AI-native companies execute them.

And in some cases, they will use that execution layer to build entirely new companies.

VI. How iValley Helps Enterprises Navigate the AI Transition

The first phase of AI was about models.

The second phase is about workflow orchestration.

Programming was the proving ground.

Enterprise operations are the real market.

The winners will not simply deploy copilots on top of existing software.

They will redesign workflows around agents.

That requires a different transformation model:

identifying high-friction, high-Opex workflows,

redesigning them for agentic execution,

connecting enterprise data and context,

integrating orchestration layers with existing systems,

selecting the right model and AI-native partners,

and building toward domain-specific intelligence layers over time.

This is not a chatbot strategy.

It is an operating-model transformation.

For banks, fintechs, and enterprises, the question is no longer whether to “use AI.”

The question is:

Which workflows should be transformed first — and what architecture gets you from AI assistance to AI-native execution?

That is where iValley is focused. Reach out to us at info@ivalley.co to get more information or schedule an exploratory call here.

We help enterprises move through this transformation journey — from strategy and workflow mapping to AI-native orchestration and partner execution.

Because we work closely with AI-native startup teams, model builders, and enterprise technology leaders, we can help organizations evaluate the build-versus-buy landscape, identify the right transformation partners, and move from pilots to real operating leverage.

The cloud era digitized workflows.

The AI era executes them.

The enterprises that win will be the ones that redesign themselves for that reality.

Paddy Ramanathan

Founder of iValley and Host of the FINTECHTALK™ Show (on Substack, Apple Podcast, YouTube, and Spotify)

FINTECHTALK is a leading podcast and blog covering the future of finance at the intersection of fintech, AI, and crypto. Interested in being featured on the show, amplifying your message, or exploring sponsorship opportunities? Contact us at fintechtalk@substack.com